It’s no secret that the structure of the banking system provides limited choice for retail investors looking to invest their hard earning dollars in an investment fund. The oligopolistic nature of our largest financial institutions has resulted in the outright domination of bank-owned mutual funds in the Canadian market. Consequently, our financial institutions have also done well in defining how advice is paid for by retail investors.

Today, there are largely two options for an investor to buy a mutual fund from an advisor: (1) “commission-based”, where the investor pays for advice and distribution through a single management expense ratio (MER), from which the advisor receives a part of this fee directly from the fund manufacturer, and (2) fee-based advice where an investor pays a lower MER, and separately pays a percentage to their advisor directly. The former is commonly referred to as the “A” share class, while the latter is referred to as the “F” or fee-based share class. Of the two, investor advocates have long criticized the commission-based model, pointing to the potential conflict of interest for an advisor recommending a fund that also pays them a commission. On the flip side, advocates have often praised the fee-based model, as it aligns the motivations of the investor with that of the advisor with the underlying assumption that an advisor is indifferent about what funds to recommend because they are getting paid directly for advice. This said, fee-based share classes of mutual funds are often only available to those with larger account sizes, which can preclude smaller investors from investing and receiving advice.

All this said, Morningstar’s data has shown a distinct shift away from commission-based advice over the last decade.

At the end of 2024, assets invested in commission-based share classes of mutual funds were still in the majority, but only by a slight margin (48% fee-based, 52% commission-based). This is a stark contrast to a decade ago, when commission-based share classes were the norm.

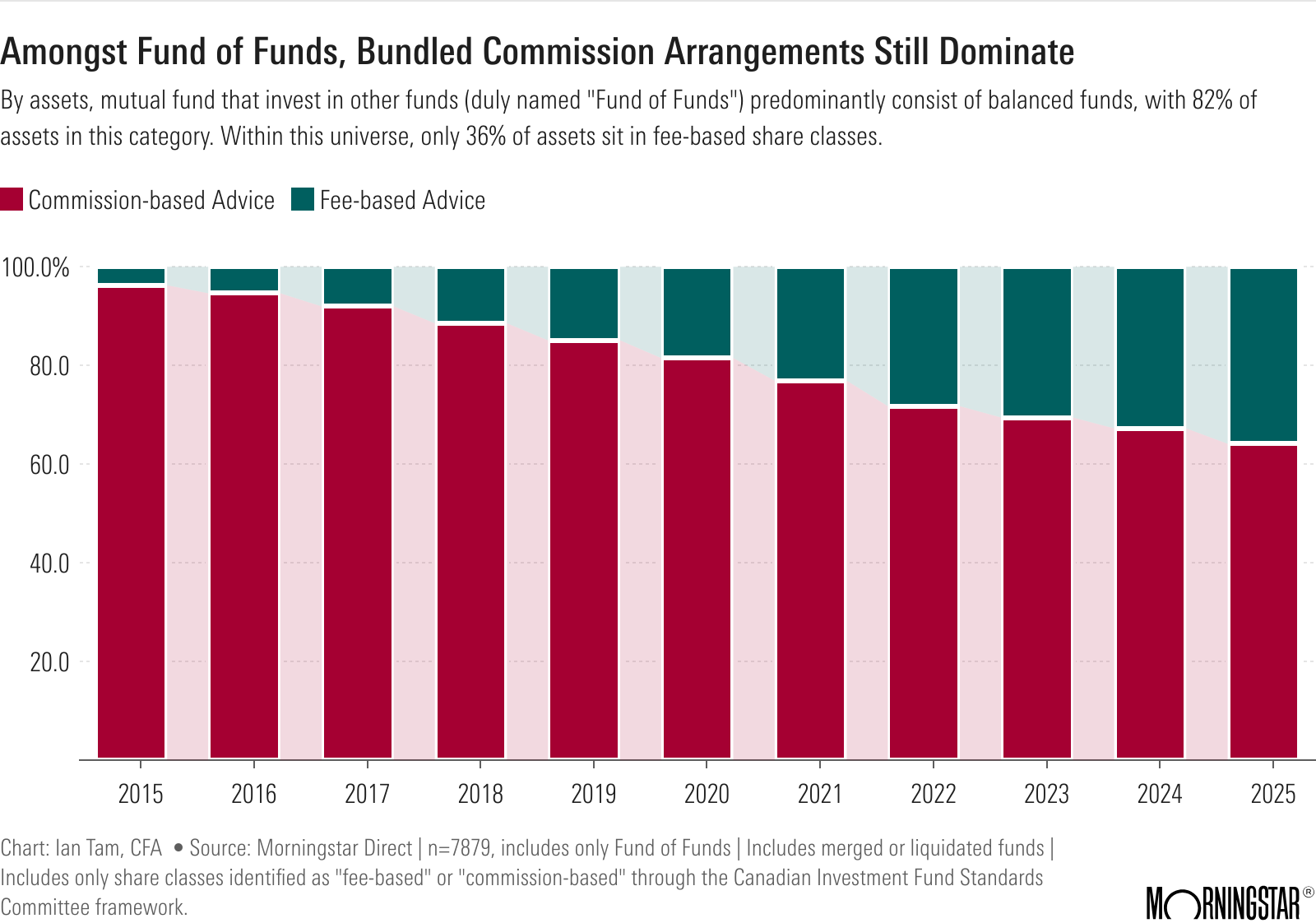

To avoid double-counting of assets, the first chart excludes “fund of funds” or mutual funds that invest in other mutual funds or ETFs. However, when we only focus on Fund of Funds (which predominantly consist of balanced funds), the data tells a much weaker story.

Today, amongst fund of funds, fee-based share classes still only make up about 36% of assets. Given that 82% of fund of fund assets in the above chart are single-ticked balanced funds often recommended by the same institutions that dominate our market, Canadian investors still have a way to go before fully decoupling commissions from advice fees.

The shift away from the bundled commission structure can be at least partially attributed to the increased transparency of fees in Canada over the last decade through regulation. Initiatives like the Client Relationship Model (CRM2) and subsequently the Client Focused Reforms have shone a light on the advice model in Canada. The shift toward fee-based advice might very well be amplified further in 2027 when client statements in Canada must adhere to a new format (dubbed “Total Cost Reporting”) which will further spell out how much is paid to advice-givers in commission-based arrangements.

This article does not constitute financial advice. Investors are encouraged to conduct their own independent research before buying or selling any investment fund or security.

Ian Tam, CFA is Director of Research at Morningstar Canada. Tam is also a member of the Ontario Securities Commission Investor Advisory Panel, and the CFA Institute ESG Technical Committee.

Discussion