RDSP Decumulation Part III A

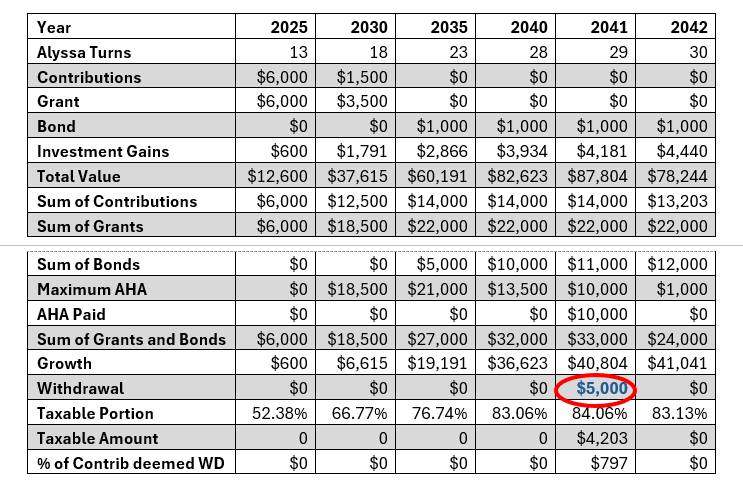

o Example: For the sake of argument, Alyssa’s RDSP goes 10 years after 2031 with no additional funding. Alyssa elects for a Disability Assistance Payment (withdrawal) of $5,000 in 2041.

So far, we’ve looked at the intent of the RDSP and how to accumulate funds in the RDSP. For the 3rd part in our series, we’ll introduce concepts related to decumulation and the RDSP.

There are 3 ways to withdraw funds from the RDSP:

|

|

Acronym |

Summary |

Triggers

Repayment of Grants and Bonds (AHA) |

|

Disability

Assistance Payment |

DAP |

One-off

payment prior to age 60 |

Potentially

yes |

|

Lifetime

Disability Assistance Payment |

LDAP |

Retirement

income starting at age 60 |

No |

|

Specified

Disability Savings Plan |

SDSP |

Payments in

case of terminal illness |

No |

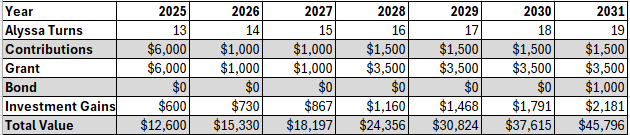

We’ll look at each of these in some detail, followed by a short case study based on the one we started in Part II of this series. It maybe helpful to once again provide the table we developed for Alyssa’s RDSP in that article:

Before we look at the three types of withdrawals, there are three other concepts we must cover. Those are:

· Assistance Holdback Amount (AHA): The potential requirement to repay grants and bonds in the case of certain withdrawals. The AHA can generally capture any grants or bonds received in the 10 years prior.

o Example: In Part II of this series, we introduced Alyssa and her RDSP. We saw her at age 19 with a $45,796 in her RDSP. Of that value, $22,000 came from grants and $1,000 from bonds, for a total of $23,000. All that money was received within the prior 10 years. If Alyssa were to withdraw any amount from her RDSP at age 19, those grants and bonds are potentially forfeit.

o In the case of a normal withdrawal (a DAP, in this case), the repayment is $3 for every $1 withdrawn, regardless of the actual amount of grants or bonds received, to the maximum of the $23,000 in question. That grant and bond entitlement is permanently lost.

o If Alyssa were to wait until 2036 to make her first DAP withdrawal, the $6,000 of grants received in 2025, when the plan was initiated, would not be subject to AHA.

o In the case of Alyssa’s death, the plan being collapsed, or the plan being deregistered, the full amount of AHA is repaid.

· *NERD ALERT* The next section is only tolerable to those who are 8/10 nerds or greater (worse?). If that’s not you, skip to “Taxation of Withdrawals”, below. *NERD ALERT ENDS*

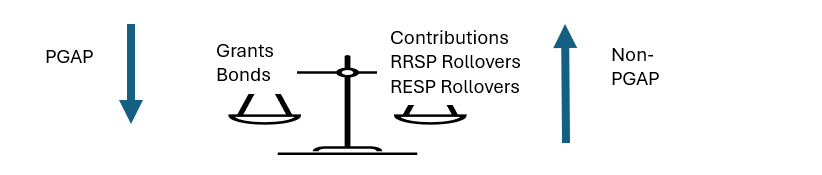

· Primarily Government Assisted Plan (PGAP): An RDSP where the majority of invested funds (as opposed to growth on those funds) originates from grants and bonds. The alternative to a PGAP is a non-PGAP.

o Example: On Jan 1 of 2031, Alyssa’s plan has $18,500 (the 2031 grants and bonds have not yet been paid) of grants and bonds, and $12,500 of contributions. This is a PGAP, as the Grants and Bonds outweigh the contributions.

o Because Alyssa’s plan is a PGAP, if she takes a DAP, that DAP is limited to the greater of 10% of the RDSP market value or that same 10% plus any contributions (not grants or bonds) withdrawn in the year plus any LDAP made in the year.

o If her plan were a non-PGAP, then there is no maximum withdrawal. (This doesn’t mean she’s free from AHA considerations, though.)

o The PGAP/non-PGAP consideration is seldom an issue. Where it is most likely to show up is when an RDSP is the recipient of a significant RRSP rollover. In such cases, there are additional planning considerations that we will cover in a future article.

· Taxation of Withdrawals: Withdrawals are taxed similarly to what happens with an RESP. After-tax contributions are withdrawn on a non-taxable basis. Any previously untaxed amounts (grants, bonds, investment gains, rollovers of investment gains from an RESP, and rollovers from an RRSP) are taxable. The taxable amount of a withdrawal is taxed on a proportional basis.

o Example: For the sake of argument, Alyssa’s RDSP goes 10 years after 2031 with no additional funding. Alyssa elects for a Disability Assistance Payment (withdrawal) of $5,000 in 2041.

o The amount withdrawn is $5,000. The taxable portion of 84.06% is based on the proportion of previously untaxed amounts (grants, bonds, growth, plus previously untaxed rollovers from other registered plans) to the overall value of the plan. That’s $73,804 against a plan value of $87,804. Only the $14,000 of contributions to this point has been previously taxed.

o 84.06% of $5,000 is $4,203, which is taxed as ordinary income to Alyssa.

o Even though contributions ceased more than 10 years ago, Alyssa has continued to receive Bonds during that time. That means the Assistance Holdback Amount is triggered. The AHA is 3 times the amount withdrawn, to the maximum of all grants and bonds received in the prior 10 years. 3 times $5,000 is $15,000, but the AHA is only $10,000, as that’s the sum of the prior 10 years of bonds. Alyssa will lose those bonds, and they will count against her lifetime maximum of $20,000 of bonds. The DAP does not prevent the present year's bond from being paid into Alyssa's RDSP.

o Because the AHA is directly held by the plan sponsor, there is no lag time in reporting the DAP and waiting for CRA to assess. The AHA is transferred from the plan sponsor to ESDC immediately after the DAP is paid.

o Depending on the province, this may also cause a reduction in that year’s provincial disability supports. Alyssa’s advisor should counsel her on the potential income loss caused by this withdrawal.

o The ‘Sum of Contributions’ is reduced by the proportion of withdrawals deemed to be a return of taxable amounts. The $797 of her withdrawals that is not taxable subsequently reduces the ‘Sum of Contributions’ calculation for any future tax considerations.

Now that we’ve spent a very enjoyable few minutes looking at the very simple, not-at-all-complicated, friendly-to-those-managing-the-affairs-of-a-person-with-a-disability, rules concerning withdrawals, the next article will focus on the first of two scenarios where withdrawals fit within the intent of the plan.

Discussion