RDSP Decumulation Part III C

We hope it doesn’t happen, but should Alyssa be diagnosed with a terminal illness, she may qualify to convert her RDSP to an SDSP.

This is a continuation of my prior RDSP article concerning withdrawals.

Specified Disability Savings Plan

We hope it doesn’t happen, but should Alyssa be diagnosed with a terminal illness, she may qualify to convert her RDSP to an SDSP. This requires that a qualified medical practitioner (MD or Nurse Practitioner) provides an opinion that she is likely to die within 5 years, and that the holder of the RDSP provides this opinion and elects to their RDSP sponsor that they wish to convert the RDSP to an SDSP.

A few rules concerning the SDSP:

· No further contributions, grants, or bonds will be paid at that point.

· If the beneficiary doesn’t die within 5 years, the plan continues to be an SDSP.

· There is no AHA paid back with respect to SDSP withdrawals, as long as the taxable amount of SDSP withdrawals is no more than $10,000. Withdrawals cannot, however, cause the plan balance to fall below the AHA. (It is still possible to trigger the AHA payback if the taxable amount of withdrawals in a year exceeds $10,000.)

· For plans with smaller values than Alyssa’s, where it would be challenging to hit the $10,000 taxable withdrawal limits, and the plan is a PGAP, there are additional restrictions concerning withdrawals. These rules are complicated (unlike the rest of this, which is so simple) and should be explored on a case-by-case basis.

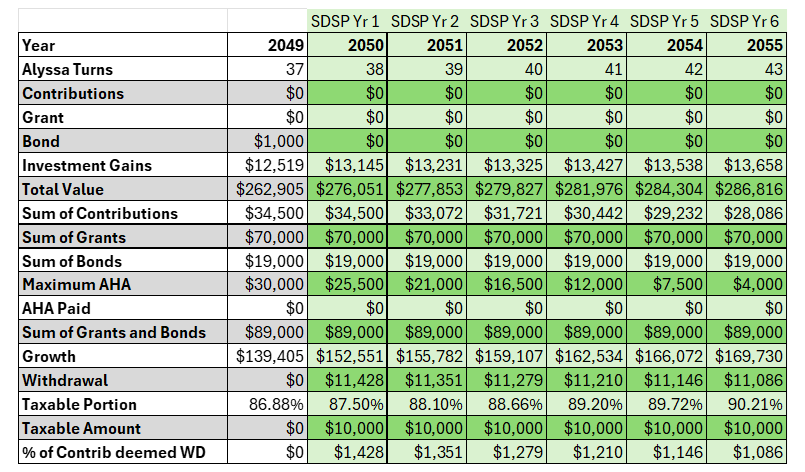

Let’s have a look at how an SDSP might work for Alyssa. Tragically, a medical doctor is willing, in the year Alyssa will turn 38, to provide a written opinion that she is likely to die within 5 years. That year, she elects to have her RDSP converted to an SDSP and begins taking income. She takes the maximum income allowed in each year and lives for another 5 years (meaning her SDSP is in effect for 6 years in total).

A few things to note:

· The amount withdrawn each year is calculated to create $10,000 of taxable income for Alyssa. That’s the maximum permitted to retain SDSP status.

· No AHA is required to be paid.

· She will likely die with a substantial estate value. As previously discussed, and as will be elaborated in a future article, this is not necessarily ideal with the RDSP.

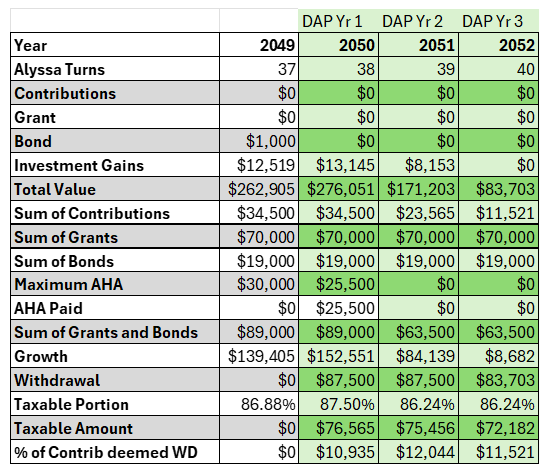

She could collapse the plan and take the full value out, less any Assistance Holdback Amount. That might be preferable. If she were to do that:

· The $25,500 of AHA would be repaid.

· She would receive $237,405 of withdrawals.

· Her taxable income would be quite high, at $206,251.

It would likely be preferable to spread withdrawals out over 2-3 years and keep her taxable income lower:

· On a 3 year withdrawal schedule, she might take approximately $87,000 of DAPs per year, keeping her taxable income near $75,000 in each of those years.

Conclusion

I was intending for the sum total of the RDSP Decumulation article to come in at about 3 pages when I first started writing this. In total, it comes to 9 pages, including tables. This is intense. I hope this illustrates:

· That there is merit in planning around RDSP withdrawals.

· That RDSP withdrawal schedules can be complicated.

· That we all (including me) have much to learn about RDSPs.

Stick with me as I continue this series. Part IV, which will be shorter, will deal with some special circumstances (the niche rules, such as loss of DTC eligibility) concerning RDSPs.

Discussion