You NEED Alternative Investments... or so I'm told. Part II

There's a subtle progression that Canadians have in the way they approach wealth management.

Early on it's about paying off student debt and getting those first contributions into their savings.

As long as the investments are sensible enough, the relative performance between investments is generally of much lower impact than the amount they're saving.

Life gets more serious at some point, and we start looking for more of a plan. People are crossing the threshold of blindly saving to be the most important thing to creating an overall plan and system to implement that plan that balances the here and now with what they want to achieve in the future.

They've grown up, and are now looking for a more sophisticated plan.

A problem with the industry is that these people are being shown things branded as 'sophisticated investments'.

This is Part II of a series on alternative investments, what they are, how they're marketed, and answer the question of 'how would these fit in when we're actually implementing a financial plan?'.

Part I can be found here.

Regardless of the type of investment – a traditional mutual fund or picking stocks/bonds, or any form of alternative investment, they are all predicated on a central commonality – buyers and sellers of investments trading amongst themselves trying to get the best price.

Buying a stock means someone else selling it to you thinks it is overvalued.

Selling a bond means the buyer thinks it is undervalued.

Whatever the transaction, if markets are efficient, meaning that anyone can move their money as they please and all buyers and sellers have equal access to information, then each buyer and seller should be acting in their own self interest to maximize the sale price or minimize the purchase price of an asset.

Are markets perfectly efficient – no, but they are close enough that the ability to have an edge or sustain such an edge is essentially nil.

Nobody is on the other side of a trade saying ‘I’m going to throw this hedge fund manager a bone on this one’.

Whether it’s traditional investments or alternative investments, the strategies are contingent on the idea that the manager is smarter than the market. They should be, right? I mean after all, that’s why they make the big bucks.

For any to be successful, the manager would need to correctly identify the future winners ‘Company A’ and losers ‘Company B’ more often than not, and generate a return greater than their fees.

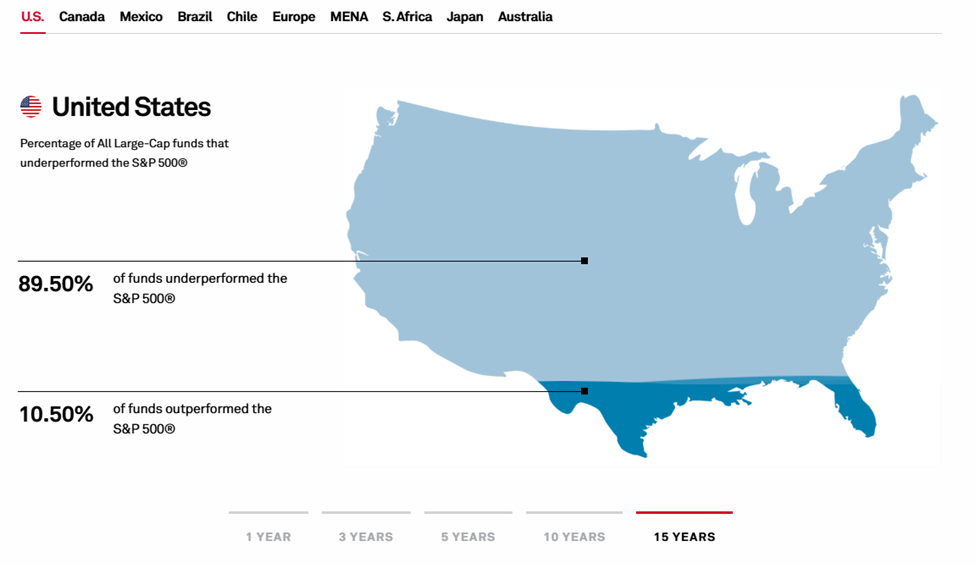

The reality is that few do.

Many studies show how long-only managers overwhelmingly underperform their benchmarks (which would include all the winning company As and losing company Bs wrapped together).

Is it luck, or is it skill?

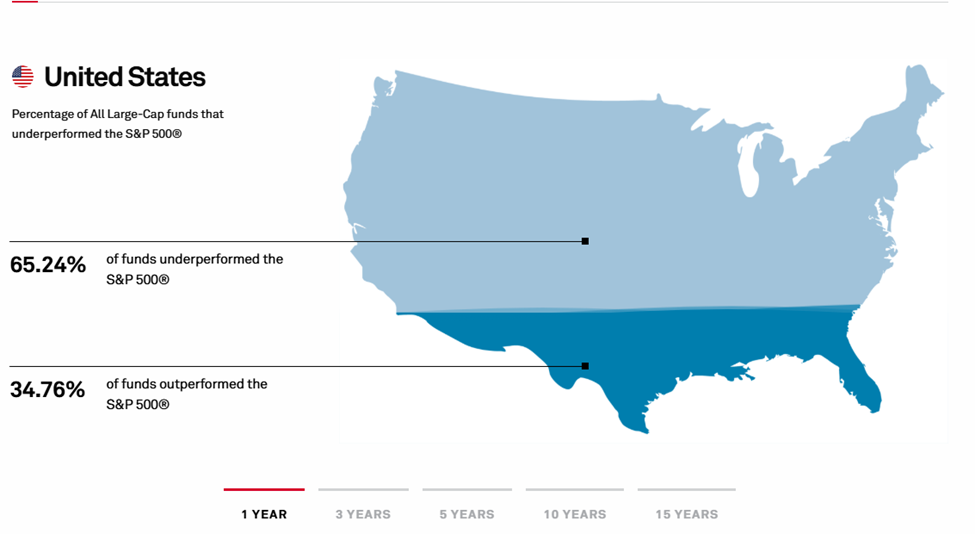

The shorter the time period, the more likely stock pickers can beat the market. Anyone can be lucky and outperform over the short-term. The longer the timeframe, the more a manager’s skill can be evaluated – how long you ask?

Eugene Fama and Kenneth French in their 2010 paper ‘Luck versus Skill in the Cross-Section of Mutual Fund Returns’ found that it you would need about 30 years to have a decent change of knowing for sure if a manager was truly skilled.

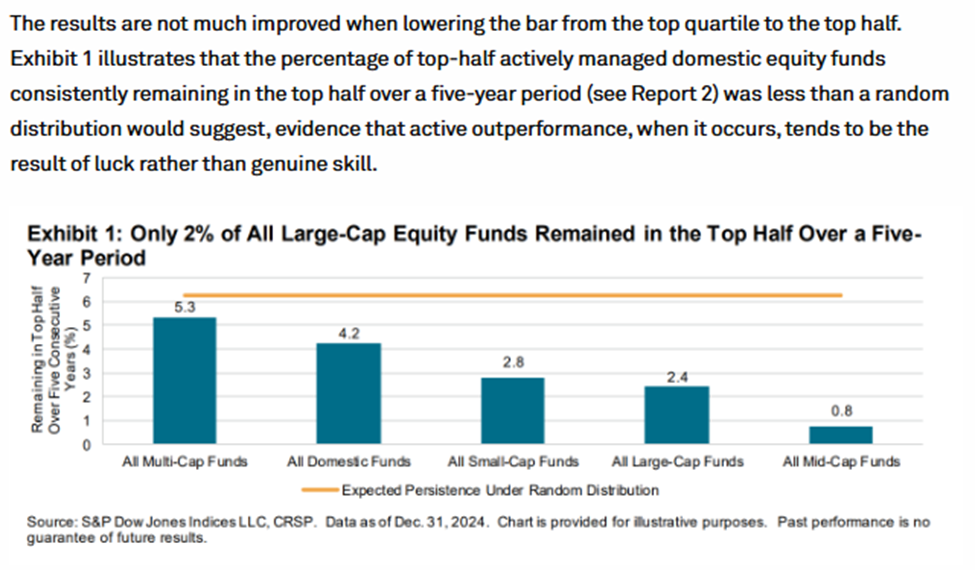

This makes extrapolating a past ‘winning’ manager into the future difficult, if not nearly impossible. The SPIVA Persistence Scorecard shows the amount of mutual fund managers who were in the top quartile that remain there in subsequent periods to be less than that of random chance – not good news for these managers, and terrible news for anyone branding themselves as advisors who can identify such winners ahead of time.

This is important to think about as we dig deeper into the world of alternative investments – the additional bells and whistles that they use to invest are nothing new or unique that only their approach to finding winners and losers is a master in.

Over any short-term there will be strategies and approaches that do better or worse than others.

But here’s the thing – the funds that clients are recommended typically have had good performance in the past. Studies have shown that investors pile into funds after that fund has shown strong performance. Why? Advisors tell clients exactly what they want to hear – “you’re a winner, this fund is a winner let’s all be winners.” Without a word of context around how unlikely that is to be the case.

If you watch the CBC Market Place video on going undercover at the big 5 Canadian banks from 2024 – you’ll see versions of this pitch in real time – yikes.

It's done because they know it works.

The easiest answer to the question “I’m looking for an investment with good performance” is to show a prospect an investment that has had great performance, and leave out any and all context.

To recap – most managers don’t outperform. It’s easier to outperform over short periods, increasingly harder over long periods as the ability to remain lucky eliminates more and more contenders. It takes 30 years to understand if a manager is truly skilled or lucky, and most advisors are still putting investments in front of their clients based on recent outperformance.

Which brings us to how alts are REALLY pitched, and why the shiny object du-jour needs to be approached with a grain of salt.

Clients aren’t being shown the alt funds with poor past performance, just like they’re not being shown the traditional equity or bond funds that have had bad performance.

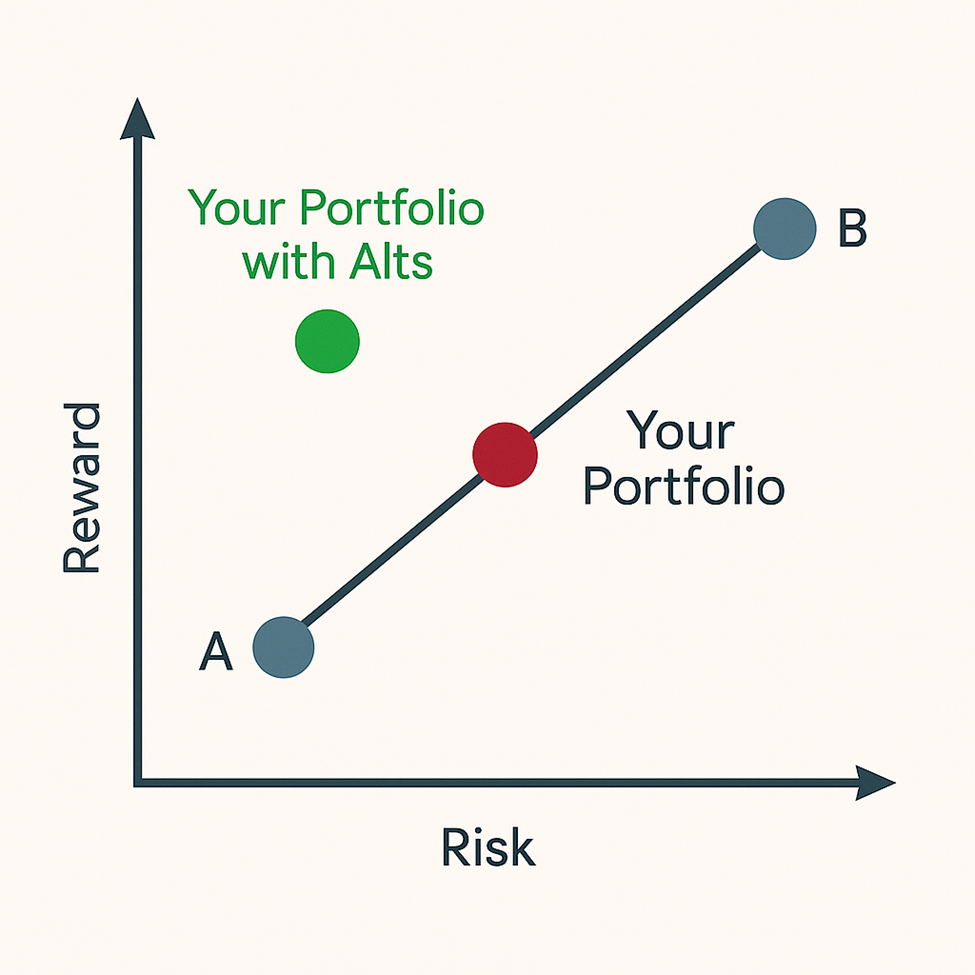

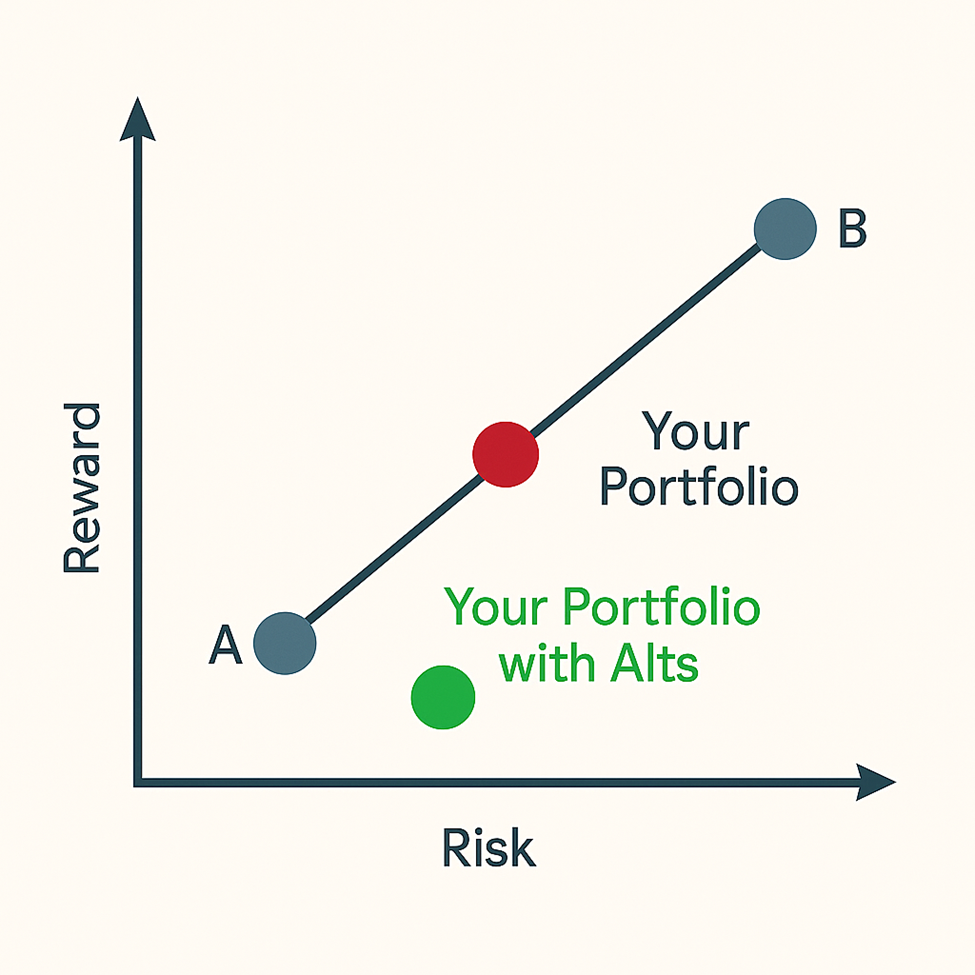

Investors are shown a good performer. Whatever the alt strategy, what the client is going to see is how adding XYZ investment will reduce the overall portfolio volatility and/or increase the returns of the portfolio, something like this:

The problem with this type of pitch is that what clients are really being shown is a zombie apocalypse movie – what you’re seeing are the humans who have not become zombies yet. It’s too soon to know which are the true survivors, and which ones have just been lucky so far.

Investors are not being pitched one that is already a zombie and would show lower the returns and/or increase the volatility, those ones don’t make the cut in the same way that a vacation brochure shows the ocean front views, not the view of the hotel next door that is under construction.

Clients and investors should always keep their eyes open when they see pitches that show great past performance.

Marketing departments aren’t taking out ads for their poor performing funds.

Being smarter than the markets is not a viable strategy over the long-term, despite what anyone may tell you.

This post was largely about setting the table on how we should think of investments. In subsequent posts I will address different types of popular alternative investments, how they work, and where they would fit in from a financial planning perspective.

Discussion